Insurance Guide

Condo and Homeowner Association (COA/HOA) Insurance Basics

Insurance Guides

Understanding Landlord Insurance in California (2026)

What landlord insurance in California covers, what it costs in 2026, and how wildfire, earthquake, and Tenant Protection Act change what you actually need.

What is a Rent Concession? 2026 Guide for Landlords

Learn what a rent concession is, when to offer one, how it affects effective rent, and the insurance risks landlords often miss. Get practical tips for smarter leasing decisions.

What is Excess Liability Insurance? A Landlord’s Guide to Higher Liability Limits

What is excess liability coverage? Learn how it works for landlords, what it costs, and when your base liability limits may not be enough.

Understanding the Different Types of Landlord Insurance

Confused about landlord insurance? Learn all about the four main policy types to help choose the best coverage for your rental property in 2026.

Knob and Tube Wiring and Insurance: What Property Owners Should Know

Knob and tube wiring is an outdated and potentially unsafe electrical system, leading to high policy premium rates and often refusals to any property with K&T wiring

Additional Insured Explained: Meaning, Benefits, Costs & Use Cases

Learn what “additional insured” means in insurance, why it matters, how much it costs, who’s eligible, and real examples of how coverage works.

What is a Squatter? 2026 Guide for Property Owners

Discover what a squatter is and how to handle them with our 2026 guide for property owners. Understand squatter rights, their meaning, and possible prevention strategies.

Staying Cool: What Are a Landlord’s Responsibilities Regarding AC?

In hot climates, having an AC or a cooling system is essential, even for rentals. It can also have a big impact on how lucrative the rental property is.

What is Condo Association Insurance?

Discover what condo association insurance is and why you may need it. Learn how it can help protect your building and community.

Mold in Rental Property: Who Needs to Fix It and How to Prevent It

Many landlord insurance policies have a fungi or bacteria exclusion, meaning that they specifically do not provide coverage for issues related to mold.

Rent Ledger: What It Is, How to Use One, and a Free Template

Learn what a rent ledger is, why it matters, and how to use one. Download a free rent ledger template for landlords, tenants, and property managers.

Ordinance or Law: ABC Coverage

Ordinance or law is a type of coverage that protects you when you need to rebuild your property according to updated building codes, ordinances and laws

Pest Control in Rental Properties: Who Has the Main Responsibility?

Pests can be a real nuisance in any home, but who's responsible for getting rid of them? The answer depends on your lease agreement and where you live.

The Landlord's Checklist for Tenants Who Are Moving Out

Tenant moving out? Here's a free, printable tenant move-out checklist saves you time and streamlines so you can get your rental unit filled again immediately

Meet Honeycomb's CEO at ITI NYC 2024, The World's Leading Insurtech Conference

Itai Ben-Zaken will join the "Perfecting Pricing: Mastering Precision to Ensure Profitability" panel, showcasing Honeycomb's unique approach to Real Estate Insurance

Landlord-Tenant Laws in New Jersey

Learn about New Jersey’s landlord-tenant laws, including landlord rights, tenant protections, rent control, eviction rules, and landlord insurance requirements.

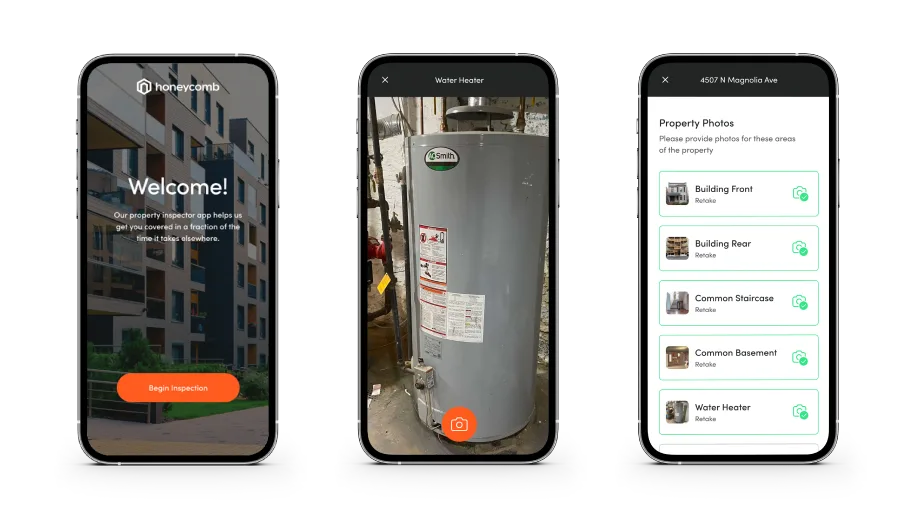

Get started with the Honeycomb Inspector App

The honeycomb inspector app is a powerful tool we use to get you covered in a fraction of the time it takes elsewhere.

Add the letter to the text boxes to update values.

Padding Values:

[ none ]

[ sm - 80 ]

[ md - 96 ]

[ lg -120 ]

[ xl - 144 ]

[ xxl -160 ]

Inner Spacing Values:

[ none ]

[ xs - 64 ]

[ sm - 72 ]

[ md - 80 ]

[ lg - 88 ]

[ xl - 96 ]

Padding Values:

[ none ]

[ sm - 80 ]

[ md - 96 ]

[ lg -120 ]

[ xl - 144 ]

[ xxl -160 ]

Inner Spacing Values:

[ none ]

[ xs - 64 ]

[ sm - 72 ]

[ md - 80 ]

[ lg - 88 ]

[ xl - 96 ]

.webp)